Content navigation

Key Takeaways

- The FTSE All Share has averaged an annual return of almost 15%1 over the past five years, yet the market remains attractively valued compared to global peers.

- Amid a backdrop of supportive monetary policy and ongoing rate cuts, larger-cap stocks have surprised by outpacing mid and small caps over 2025.

- The UK’s reliable dividend yield and increasing prevalence of share buybacks continue to provide robust shareholder returns, while government initiatives may boost domestic investment and support further market recovery.

Strong Year for UK Equities

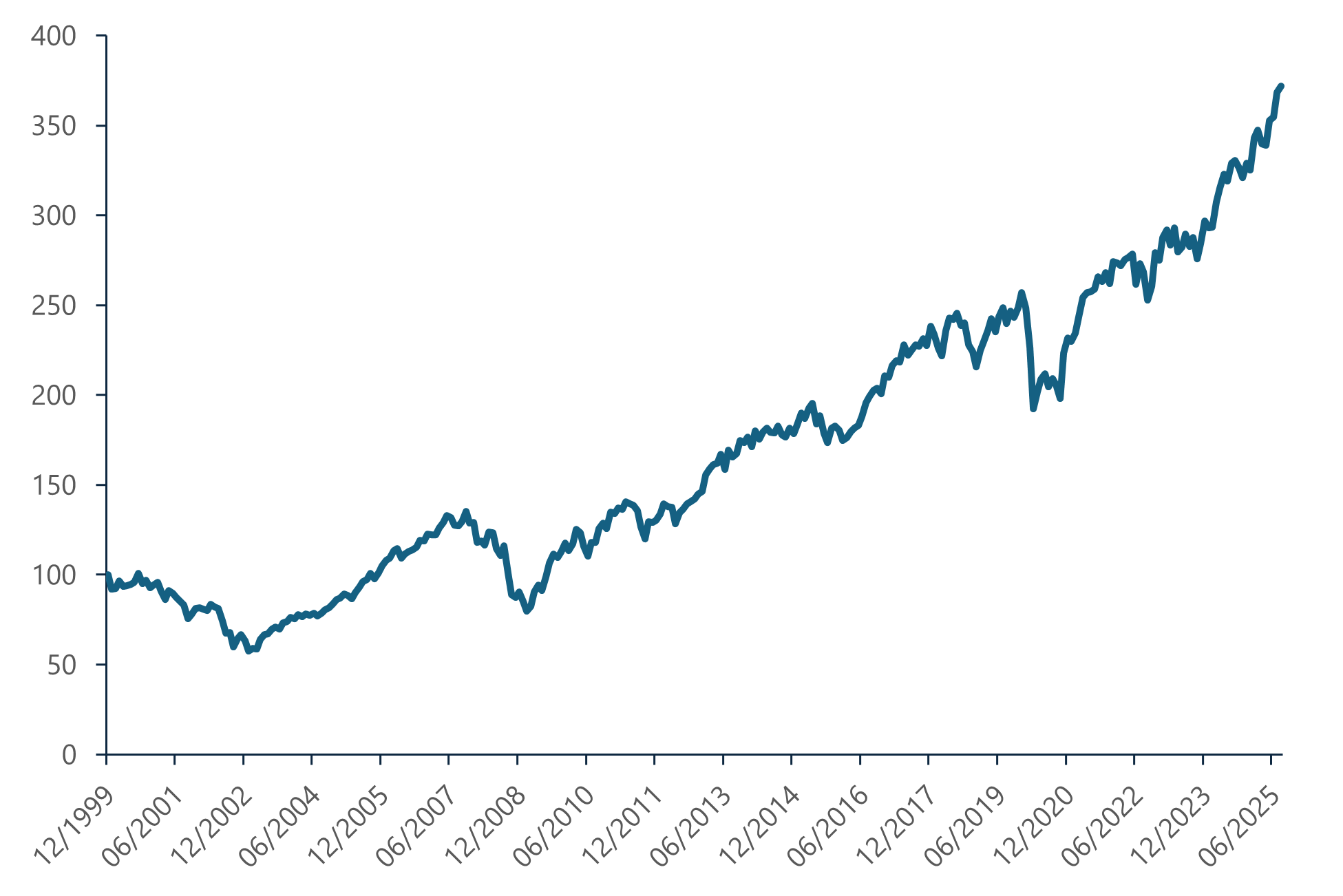

UK equities have been one of the top performers in global equity markets over 2025, with the market providing a return of almost 20%2. This isn’t a one-year phenomenon, the FTSE All Share has returned almost 15% annually for the past five years. Yet, it’s a market that continues to look like good value by any international comparison.

At the larger end of the market, the FTSE 100 with its global powerhouses across banking, healthcare, mining and energy industries, has been charging ahead. The benefit of an internationally exposed market, sterling holding steady and all whilst looking attractively valued has not been overlooked by investors. These companies have continued to demonstrate earnings growth which has been further enhanced by the increasing use of share buybacks by UK-listed companies. And investment performance hasn’t been confined to the larger end of the market. The charge from the FTSE 100 has outpaced mid and small cap stocks but they have both produced positive returns for the year.

Exhibit 1: FTSE All Share – Total Return (Indexed)

Source: Bloomberg at at 31 October 2025.

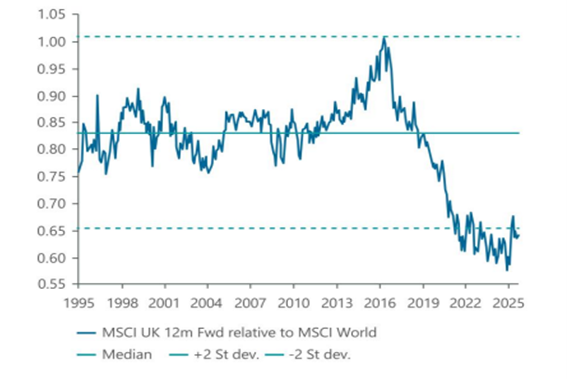

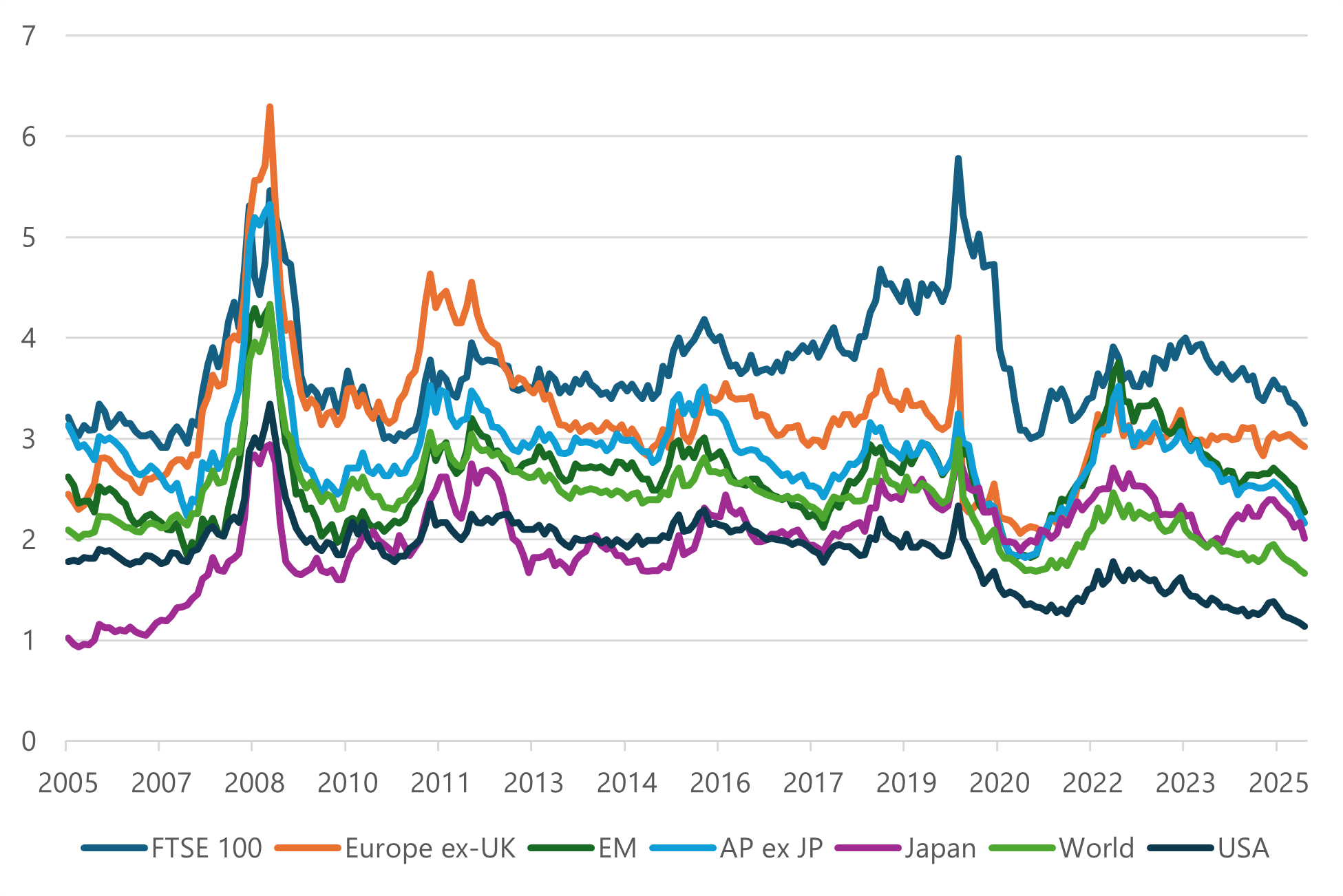

Exhibit 2: MSCI UK 12m forward P/E relative to MSCI World

Source: JP Morgan as at 3 November 2025

-

"UK equities have been one of the top performers in global equity markets over 2025, with the market providing a return of almost 20%."

Foothills of recovery

The exciting part of the UK’s recent performance is that many of the same past drivers of returns remain true looking forward. Although UK equity markets have had a strong year, ClearBridge believes we are only in the foothills of a market recovery. The economic environment has been ready, like a coiled spring, on the verge of a recovery for a couple of years. Inflation has peaked and should continue to reduce over 2026, real wage growth has offset this pressure, the interest rate cutting cycle has begun, and savings rates are elevated; yet, stuttering confidence and an uncertain political backdrop have been road blocks to a fully-fledged UK resurgence.

Interest rate cuts are normally an early sign the economy is moving towards a domestic recovery. Throughout 2025 the Monetary Policy Committee (MPC) voted for three rate cuts with it finely in the balance if there will be one more at the December MPC meeting. Under this backdrop, based on historic market performance, we would have anticipated mid and smaller cap stocks to outperform large caps. This hasn’t materialised. Blue chip stocks have continued to outpace the broader market due to several reasons:

- Autumn Statement 2024

The late 2024 budget was the largest tax raising in decades, targeting companies through higher National Insurance contributions and higher national minimum wage. This hit hardest for many domestic companies, squeezed company margins and put downward pressure on UK company growth expectations.

- Renewed inflation and delayed interest rate cuts

The increased taxation burden also helped fuel a secondary inflationary spike, as companies passed on some of these additional costs through to the consumer. As a result, the MPC has been divided and more tentative in the pace of rate cuts

- Negative domestic sentiment

The doom and gloom sentiment that has shrouded the UK has certainly weighed on mid and small cap stocks. Challenges remain but there are many reasons to be optimistic, and it’s easy to envisage improving UK sentiment in the year ahead.

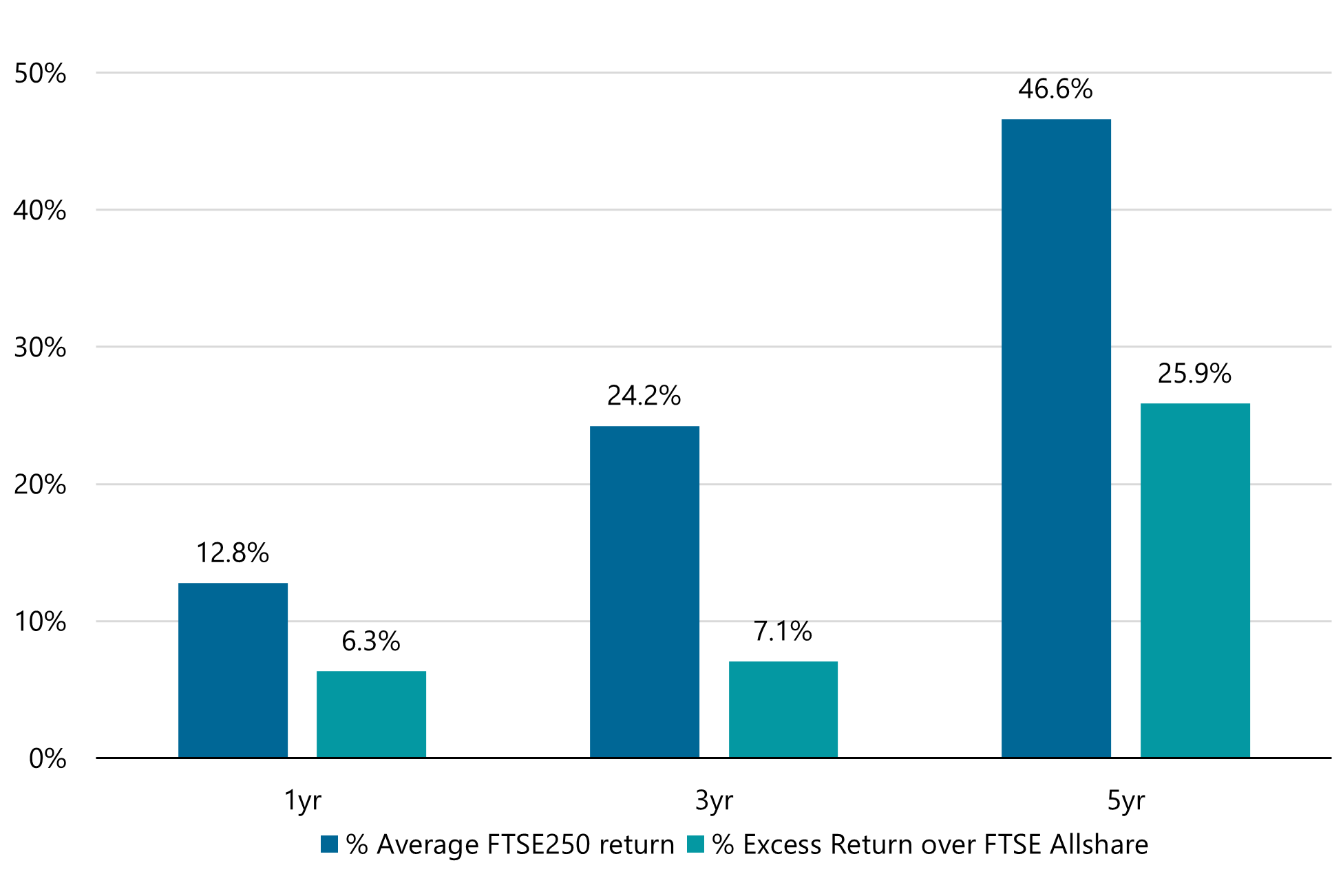

Exhibit 3: FTSE 250 Returns After First UK Interest Rate Cut

Source: ClearBridge and Bloomberg as of 31 May 2024. Data is month end index for the month when UK interest rates were first cut. Date range analysed is 1990-2024 (7 rate cut periods).

Domestic Economy: What’s Next?

On first impressions, the Autumn Statement is less inflationary and puts less pressure on employers than last year’s disastrous budget. The Office for Budgetary Responsibility (OBR) projects the UK will continue to benefit from falling inflation, which we believe will pave the way for further rate cuts and open the door for an injection of consumer confidence. Elevated levels of aggregate savings in the UK provide a further boost of optimism.

At a company level, resilient corporate earnings have resulted in healthy cash generation levels and strong balance sheets. Looking ahead, there is little reason to see anything different as management teams expertly navigate an uncertain environment. Aggregate earnings per share growth is forecast to grow at 10% in 20263, which we believe to be a realistic assessment of what companies can achieve. Over the past couple of years, the UK market has become hypersensitive to any earnings misses, with negative market swings on the back of profit warnings often proving to be significantly larger than the accompanying earnings downgrade. Realistic company guidance should help limit some of these market moves and may also aid the positive sentiment to UK markets through increased confidence in corporate forecasts.

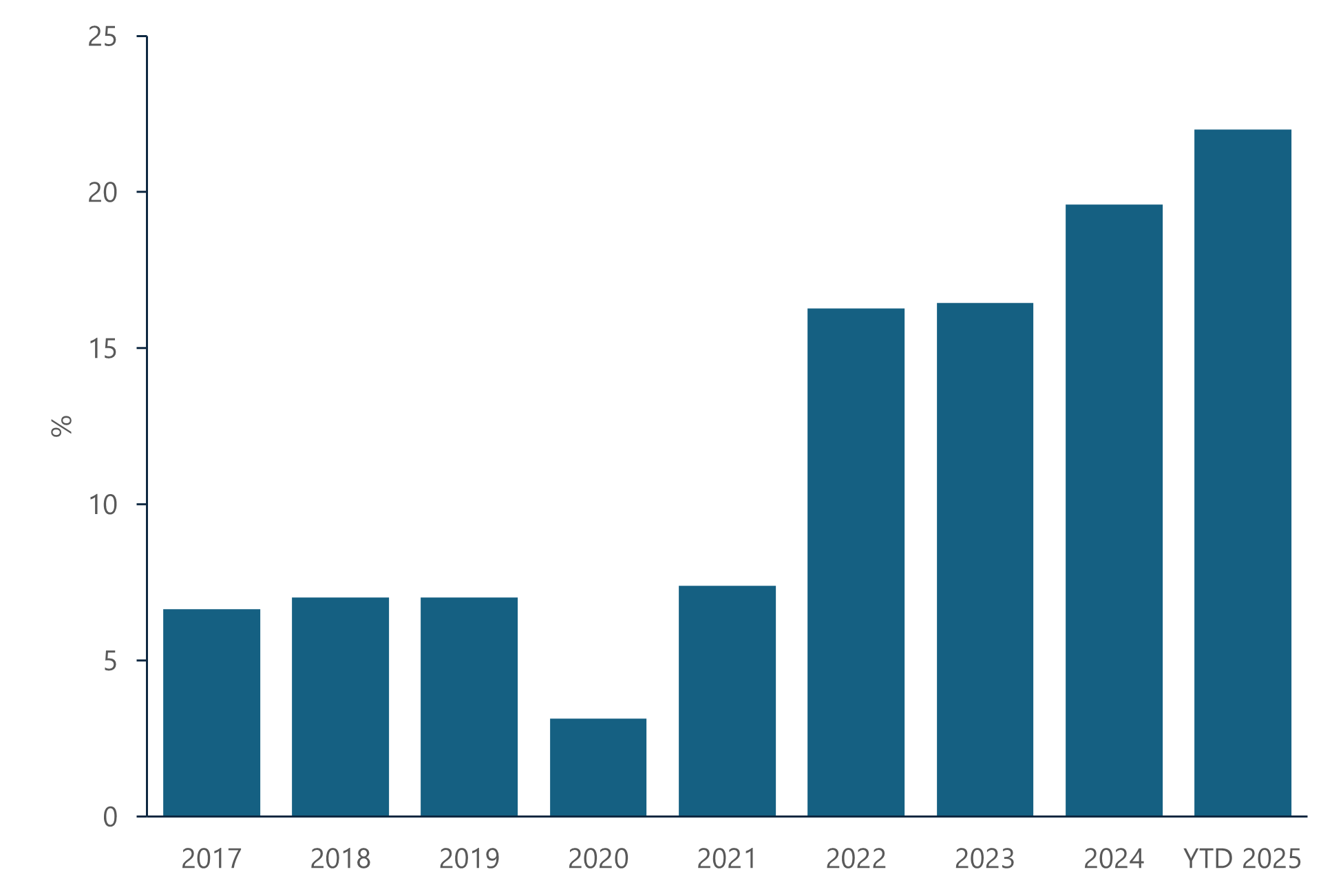

Given many UK companies are not overleveraged, whist continuing to be profitable, management teams have been looking at the best ways to return excess capital to shareholders. The UK market is famous for its reliable dividend culture and UK equities have provided a yield of almost double the global average over 2025. Management teams are also increasingly utilising share buybacks as a good use of excess cash as, whilst valuations remain appealing, share buybacks are a strong management tool in buoying shareholder returns.

Exhibit 4: Percentage of FTSE All Share Index Constituents that Repurchased at Least 1% of their Shares in each Year

Source: Bloomberg at at 28 October 2025.

Exhibit 5: Dividend Yield across the Globe

Source: FactSet as at 11 November 2025.

-

"With attractive valuations, resilient corporate fundamentals, robust shareholder returns and a supportive policy backdrop, we believe UK equities are poised to offer compelling opportunities for investors in 2026 and beyond."

Investment Style

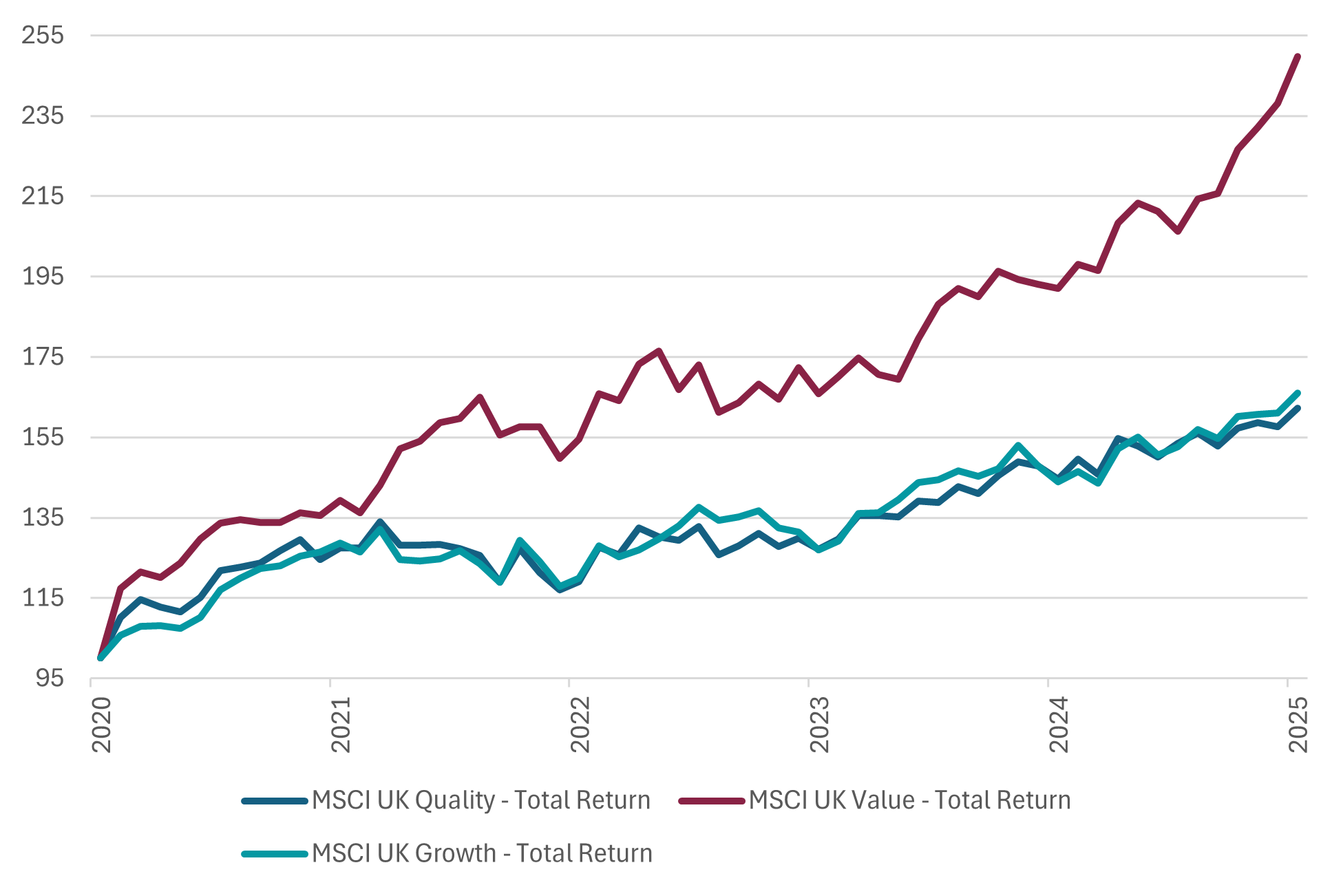

When analysing the stylistic characteristics of the market, the starkest observation is the outperformance of value overgrowth and the significant underperformance of quality over the past five years, at odds with the long-term market drivers. Quality companies, particularly those with strong balance sheets and stable earnings, typically lag the broader market in early-cycle recoveries, when markets favour cyclical and value stocks that rebound sharply from depressed levels. However, at this point in the cycle, the quality “premium” has been compressed, offering relative upside from here. As the market shifts back to focus on fundamentals, we anticipate these stocks will be more than rewarded.

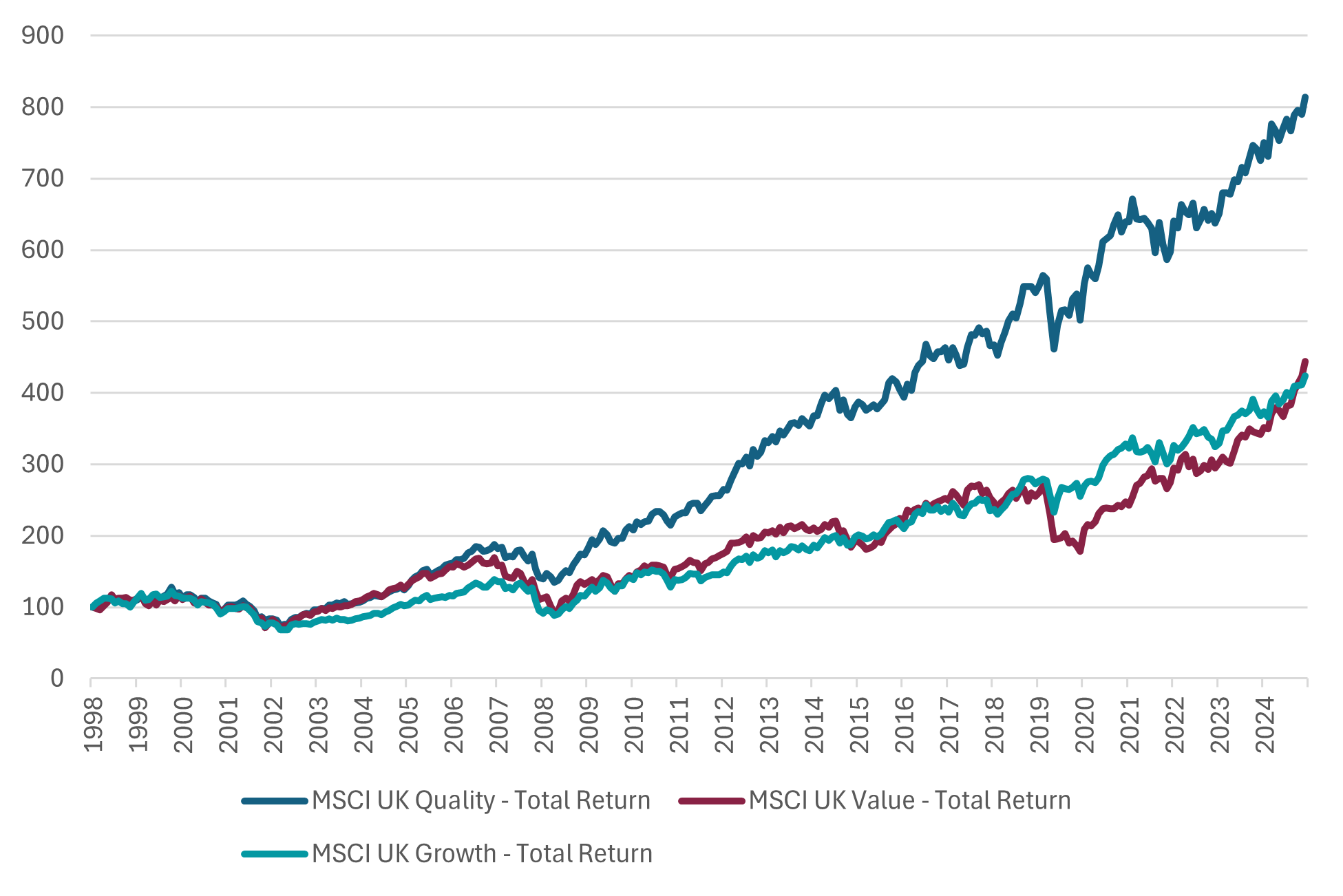

Exhibit 6: Quality Adds Value Over the Long Term

Source: FactSet 31 October 2025.

Exhibit 7: Five years Returns – Quality, Growth and Value

Source: FactSet 31 October 2025.

UK Investment Flows

UK equities have experienced multiple decades of outflows from UK wealth managers moving towards global benchmarking, and insurance companies and pension funds, with their previously large domestic allocations, which has acted to put downwards pressure on returns. The government is currently exploring ways to reverse this trend and support UK asset markets. The Mansion House Accord, signed in May 2025, was a voluntary agreement by significant defined contribution pensions providers to invest more in the UK, particularly in private markets. Further to this, the government have included a “reserve power” in the Pensions Schemes Bill that is currently passing through the House of Commons, this provides the government a legal mechanism to compel pensions investments into UK assets if voluntary efforts are not sufficient. In the 2025 Autumn Statement, the Chancellor introduced a three-year exemption for stamp duty on new main market listings, this should be supportive to the smaller end of the UK market. At the same time the government capped the cash ISA allowance, to encourage ISA equity investment, although we believe this measure will have a very marginal benefit for the UK market. Finally, the UK certainly has the inherent potential to attract international investors, who may observe improving fundamentals and look to the UK offering some of the most attractive valuations, globally.

Valuations

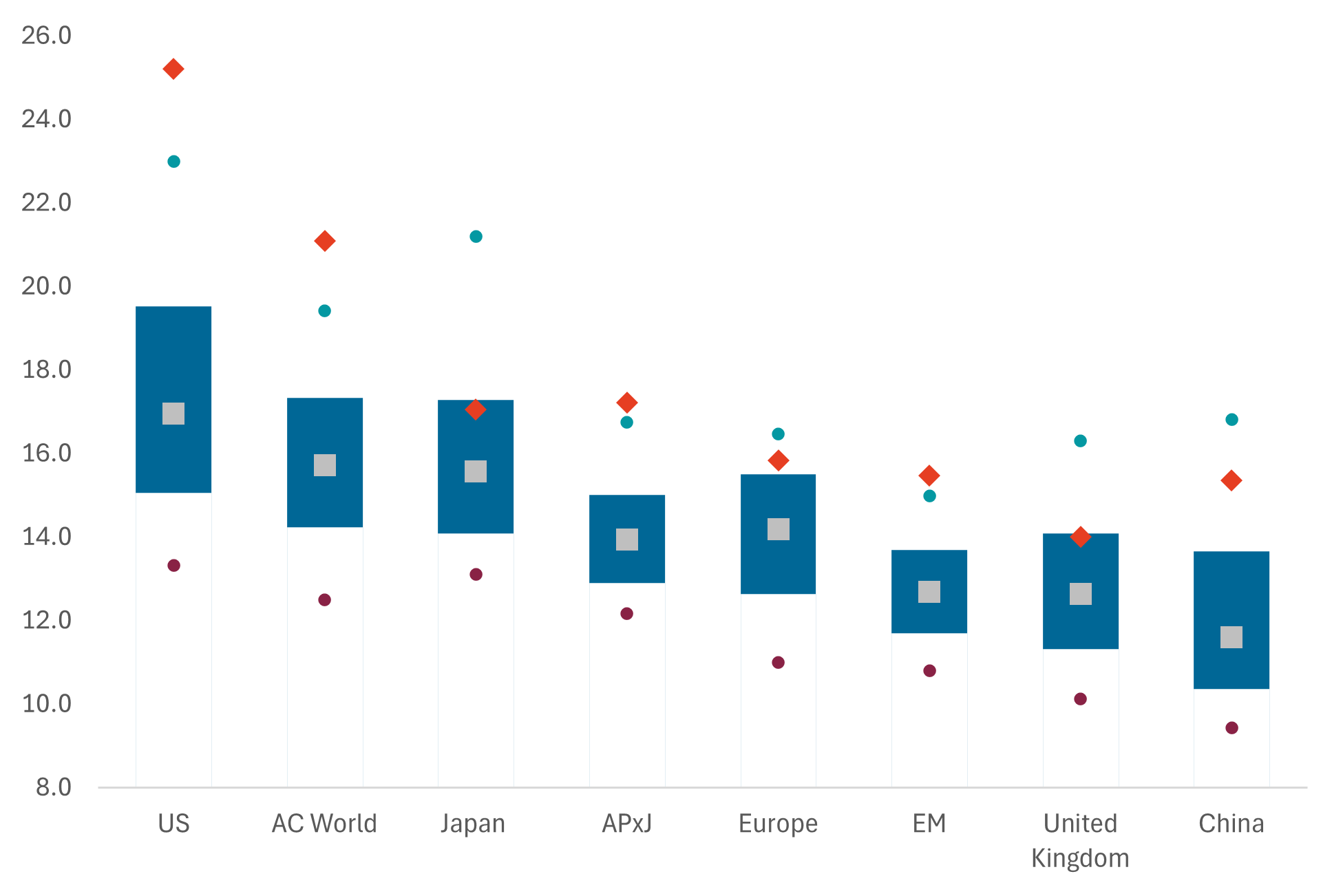

Looking across global equity markets, the UK still looks attractively valued. Especially when compared to US valuations and global allocations, currently trading above their 90th percentile price range. Moreover, international companies and private equity firms continue to target UK companies for acquisition, further reinforcing the value opportunity the UK equity market offers.

Looking across the market capitalisation of the UK market, we believe the largest valuation opportunity lies in mid and small cap companies. Following the significant outperformance of UK large caps and a prolonged period of underperformance for the UK SMid indexes, this have left valuation looking very attractive versus historic ranges and relative to the wider UK market. The FTSE 250 index currently trades on a forward P/E valuation less than the All-Share (this has historically been a premium), and the dividend yield is now higher (historically lower).

While macro and domestic pressures are likely to persist, what these discounted valuations miss, in our view, are the underlying qualities and strong fundamentals of some great British businesses, many that have shown prodigious resilience in this period of uncertainty and are poised to reassert their strong fundamentals.

Exhibit 8: Forward PE (FY1) of given equity markets

Source: FactSet as at 11 November 2025.

Time to Get Excited

With attractive valuations, resilient corporate fundamentals, robust shareholder returns and a supportive policy backdrop, we believe UK equities are poised to offer compelling opportunities for investors in 2026 and beyond - making now an exciting time to consider allocating to this dynamic and undervalued market.

Sources

1Source: FactSet as at 31 October 2025.

2Source: FactSet as at 31 October 2025.

3Source: Bloomberg as at 12 November 2025.

Important Information

This information is issued and approved by ClearBridge Investment Management Limited (‘CIML’), authorised and regulated by the Financial Conduct Authority. It does not constitute investment advice. Market and currency movements may cause the capital value of shares, and the income from them, to fall as well as rise and you may get back less than you invested.

The information contained in this document has been compiled with considerable care to ensure its accuracy. However, no representation or warranty, express or implied, is made to its accuracy or completeness. ClearBridge Investments has procured any research or analysis contained in this document for its own use. It is provided to you only incidentally and any opinions expressed are subject to change without notice.

This document may not be distributed to third parties. It is confidential and intended only for the recipient. The recipient may not photocopy, transmit or otherwise share this document, or any part of it, with any other person without the express written permission of Martin Currie Investment Management Limited.

The document does not form the basis of, nor should it be relied upon in connection with, any subsequent contract or agreement. It does not constitute, and may not be used for the purpose of, an offer or invitation to subscribe for or otherwise acquire shares in any of the products mentioned.

Past performance is not a guide to future returns.

The distribution of specific products is restricted in certain jurisdictions, investors should be aware of these restrictions before requesting further specific information.

The views expressed are opinions of the portfolio managers as of the date of this document and are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. These opinions are not intended to be a forecast of future events, research, a guarantee of future results or investment advice.

Please note the information within this report has been produced internally using unaudited data and has not been independently verified. Whilst every effort has been made to ensure its accuracy, no guarantee can be given.

The information provided should not be considered a recommendation to purchase or sell any particular strategy / fund / security. It should not be assumed that any of the securities discussed here were or will prove to be profitable.

It is not known whether the stocks mentioned will feature in any future portfolios managed by ClearBridge Investments. Any stock examples will represent a small part of a portfolio and are used purely to demonstrate our investment style.

Risk warnings – Investors should also be aware of the following risk factors which may be applicable to the strategy shown in this document.

- Investing in foreign markets introduces a risk where adverse movements in currency exchange rates could result in a decrease in the value of your investment.

- This strategy may hold a limited number of investments. If one of these investments falls in value this can have a greater impact on the strategy’s value than if it held a larger number of investments.

- Smaller companies may be riskier and their shares may be less liquid than larger companies, meaning that their share price may be more volatile.