Content navigation

Key takeaways

- Emerging markets (EM) posted positive returns, driven by Info Tech, Taiwan, and Korea

- Consumer Discretionary, Saudi Arabia, and China lagged during the quarter

- The asset class benefited from a weaker US dollar and lower interest rates

Market overview

Emerging markets delivered robust returns during the second quarter despite tariff policy uncertainty. The MSCI EM Index returned 12% and outpaced the S&P 500 (+11%) for the second quarter in a row. The asset class was driven positively by a rebound in the Information Technology sector (+24%) and a rally in Industrials (+22%), while Consumer Discretionary (-3%) and Consumer Staples (+6%) underperformed during the quarter.

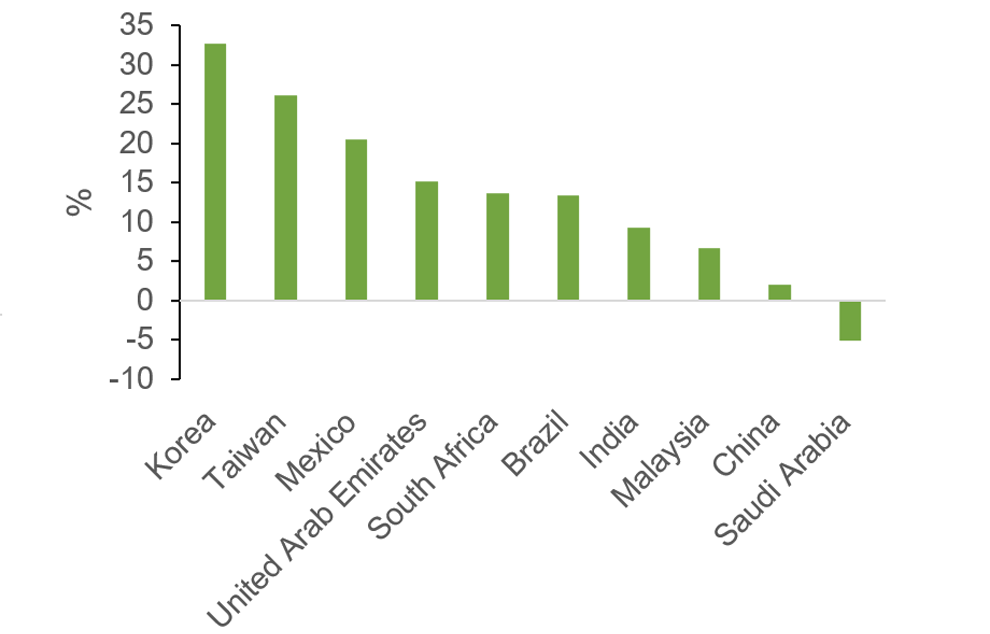

From a geographic perspective, the tech-heavy markets of South Korea (+33%) and Taiwan (+26%) posted strong returns, while Saudi Arabia (-5%) was the only market that declined during the quarter. China also lagged with a +2% return in Q2. While easing of US-China trade tensions offered some relief, many large-cap Chinese internet stocks were hurt by a backdrop of increasing competition between the key players. Notably, the US dollar weakened, which was a tailwind for EM investors.

MSCI EM core country and sector performance Q2 2025

Sector Performance

Country Performance

Source: FactSet, as at 30 June 2025. Data in US$. Countries with an index weight over 1% shown.

Top ten holdings by active weight

| Stock | Country | Sector | Active(%) |

|---|---|---|---|

| TSMC | Taiwan | Information Technology | 3.9 |

| HDFC Bank | India | Financials | 3.4 |

| Tencent | China | Communication Services | 3.4 |

| ICICI Bank | India | Financials | 2.7 |

| China Merchants | China | Financials | 2.5 |

| Titan Company Ltd | India | Consumer Discretionary | 2.3 |

| Samsung Electronicss | Korea | Information Technology | 2.3 |

| Apollo Hospitals | India | Healthcare | 2.2 |

| SK Hynix | Korea | Information Technology | 2.2 |

| Capitec Bank | South Africa | Financials | 1.9 |

Source: Martin Currie as of 30 June 2025. Data shown is for the Martin Currie Global Emerging Markets representative account. Holdings are subject to change.

Portfolio discussion

The Martin Currie Global Emerging Markets strategy benefited from an overweight to and selection within Info Tech as AI beneficiaries and leading semiconductor companies, Taiwan Semiconductor and SK Hynix, rallied during the quarter. Stock selection in the Energy sector also contributed to performance.

The key detractors for the portfolio this quarter were Industrials and China. Within Industrials, the market focused on short-term momentum-driven names in South Korea, in which we are underweight. Additionally, our Chinese consumer stocks Alibaba, Meituan, and JD.com sold off due to near-term competition especially in the food delivery space. Our long-term outlook remains positive for these companies.

Portfolio activity

We added four companies to our clients’ portfolios in the second quarter:

Clicks Group: Clicks is the leading health and beauty retailer in South Africa, and it operates UPD, a leading full range pharmaceutical wholesaler. The company boasts higher returns-on-equity relative to its industry and offers predictable outcomes with a defensive business model and an appealing long-term growth profile.

Etihad Etisalat: The company, also known as Mobily, is a high-quality telecommunications operator in the Middle East. Mobily is well-positioned in the industry due to its enterprise-led growth prospects, superior capital management credentials and optionality around service offering diversification, asset sales and dividend hikes.

Inter: Inter is a popular digital bank in Brazil with strong customer engagement and around 7% of the Brazilian population as a primary customer. The company offers innovative products and competitive advantages in terms of lower costs and the lowest cost of funding in Brazil. It has very low market share in Brazilian banking and multiple growth engines. The skew toward secured lending offers asset quality reassurance and consistency of growth that is less macro-economically sensitive.

Localiza: Localiza is a Brazilian car rental company that was founded over 50 years ago. This company has been a consistent compounder over time but currently is facing a cyclical trough in profitability. The company is applying upward pricing pressure to restore profitability and should enjoy above average levels of earnings growth over the next five years.

We exited four companies:

Cosan: Cosan is a Brazilian conglomerate that produces bioethanol, sugar, and energy. The company’s exposure to cyclical businesses has been magnified by its growing balance sheet leverage. While the new management team is expected to streamline the asset structure, we favour higher-quality and lower-leverage opportunities in the region.

GlobalWafers: Global Wafers is a silicon wafer supplier based in Taiwan. With the potential weaker consumer technology market, risks of an inventory overbuild in the wafer industry have increased. This oversupply could impact wafer pricing and overall growth and profitability for GlobalWafers.

LG Chem: LG Chem is a Korean petrochemicals, advanced materials, and life sciences company. LG Chem’s petrochemical business has suffered from a prolonged downcycle that is showing little sign of abating. The company’s exposure to EV battery manufacturing is also facing tariff related uncertainty that could put pressure on both short- and long-term demand from the North American component of their client base.

Robinsons Retail: Robinsons Retail is a multi-format retailer based in the Philippines. The company has a solid retail business, but we are concerned about its strategic direction, namely the company's start-up investments are dragging profitability. Combined with reduced liquidity (both for the Philippines market and specifically Robinsons) we see no clear routes to value being unlocked.

Outlook

After an eventful first half of the year with tariff uncertainty and heightened geopolitical tensions, EM equities still delivered their strongest start to the year since 2017. While we continue to monitor these developments closely, we expect the asset class to be rewarded for strong fundamentals at reasonable valuations. Importantly, the weaker dollar has alleviated pressures on EM currencies, which has allowed for key central banks to lower interest rates. We expect this easing monetary environment to benefit our high-quality growth companies as investors turn their focus back to long-term fundamentals.

We firmly believe that the outlook for EM remains robust, and we maintain strong confidence in our portfolio holdings, particularly across IT, India, China and others. The market persistently undervalues high-quality, sustainable growth companies, and we expect that investing in these companies will have the potential to lead to positive results over time.

The information provided should not be considered a recommendation to purchase or sell any particular strategy / fund / security. It should not be assumed that any of the security transactions discussed here were or will prove to be profitable.

Important Information

This information is issued and approved by ClearBridge Investment Management Limited (‘CIML’), authorised and regulated by the Financial Conduct Authority. It does not constitute investment advice. Market and currency movements may cause the capital value of shares, and the income from them, to fall as well as rise and you may get back less than you invested.

The information contained in this document has been compiled with considerable care to ensure its accuracy. However, no representation or warranty, express or implied, is made to its accuracy or completeness. ClearBridge Investments has procured any research or analysis contained in this document for its own use. It is provided to you only incidentally and any opinions expressed are subject to change without notice.

This document may not be distributed to third parties. It is confidential and intended only for the recipient. The recipient may not photocopy, transmit or otherwise share this [document], or any part of it, with any other person without the express written permission of ClearBridge Investment Management Limited.

This document is intended only for a wholesale, institutional or otherwise professional audience. ClearBridge Investment Management Limited does not intend for this document to be issued to any other audience and it should not be made available to any person who does not meet this criteria. ClearBridge Investments accepts no responsibility for dissemination of this document to a person who does not fit this criteria.

The document does not form the basis of, nor should it be relied upon in connection with, any subsequent contract or agreement. It does not constitute, and may not be used for the purpose of, an offer or invitation to subscribe for or otherwise acquire shares in any of the products mentioned.

Past performance is not a guide to future returns.

The distribution of specific products is restricted in certain jurisdictions, investors should be aware of these restrictions before requesting further specific information.

The views expressed are opinions of the portfolio managers as of the date of this document and are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. These opinions are not intended to be a forecast of future events, research, a guarantee of future results or investment advice.

Some of the information provided in this document has been compiled using data from a representative account. This account has been chosen on the basis it is an existing account managed by ClearBridge Investments, within the strategy referred to in this document. Representative accounts for each strategy have been chosen on the basis that they are the longest running account for the strategy. This data has been provided as an illustration only, the figures should not be relied upon as an indication of future performance. The data provided for this account may be different to other accounts following the same strategy. The information should not be considered as comprehensive and additional information and disclosure should be sought.

The information provided should not be considered a recommendation to purchase or sell any particular strategy / fund / security. It should not be assumed that any of the security transactions discussed here were or will prove to be profitable.

It is not known whether the stocks mentioned will feature in any future portfolios managed by ClearBridge Investments. Any stock examples will represent a small part of a portfolio and are used purely to demonstrate our investment style.

Risk warnings – Investors should also be aware of the following risk factors which may be applicable to the strategy shown in this document.

- Investing in foreign markets introduces a risk where adverse movements in currency exchange rates could result in a decrease in the value of your investment.

- This strategy may hold a limited number of investments. If one of these investments falls in value this can have a greater impact on the strategy’s value than if it held a larger number of investments.

- Smaller companies may be riskier and their shares may be less liquid than larger companies, meaning that their share price may be more volatile.

- Emerging markets or less developed countries may face more political, economic or structural challenges than developed countries. Accordingly, investment in emerging markets is generally characterised by higher levels of risk than investment in fully developed markets.

- The strategy may invest in derivatives index futures and FX forwards to obtain, increase or reduce exposure to underlying assets. The use of derivatives may result in greater fluctuations of returns due to the value of the derivative not moving in line with the underlying asset. Certain types of derivatives can be difficult to purchase or sell in certain market conditions.

For wholesale investors in Australia: This material is provided on the basis that you are a wholesale client within the definition of ASIC Class Order 03/1099. CIML is authorised and regulated by the FCA under UK laws, which differ from Australian laws.