Content navigation

Key Takeaways

- Middle East tensions are driving volatility, creating opportunities for disciplined, long-term investors

- UK equities offer global earnings exposure with a more defensive tilt and attractive dividend profile

- Selective focus on profitable, well-capitalised companies can help navigate uncertainty and capture long-term upside

2025 was a spectacular year for UK equities, and the UK economy was entering 2026 with momentum building. Inflation appeared broadly on track towards its 2% target1, markets were pricing further rate cuts over the year ahead, and, after several years of real wage growth, consumer and business confidence had recovered to long-term averages. After a prolonged period of sluggish activity, the UK finally looked set to regain traction. However, recent developments in the Middle East have reshaped the outlook for the year ahead.

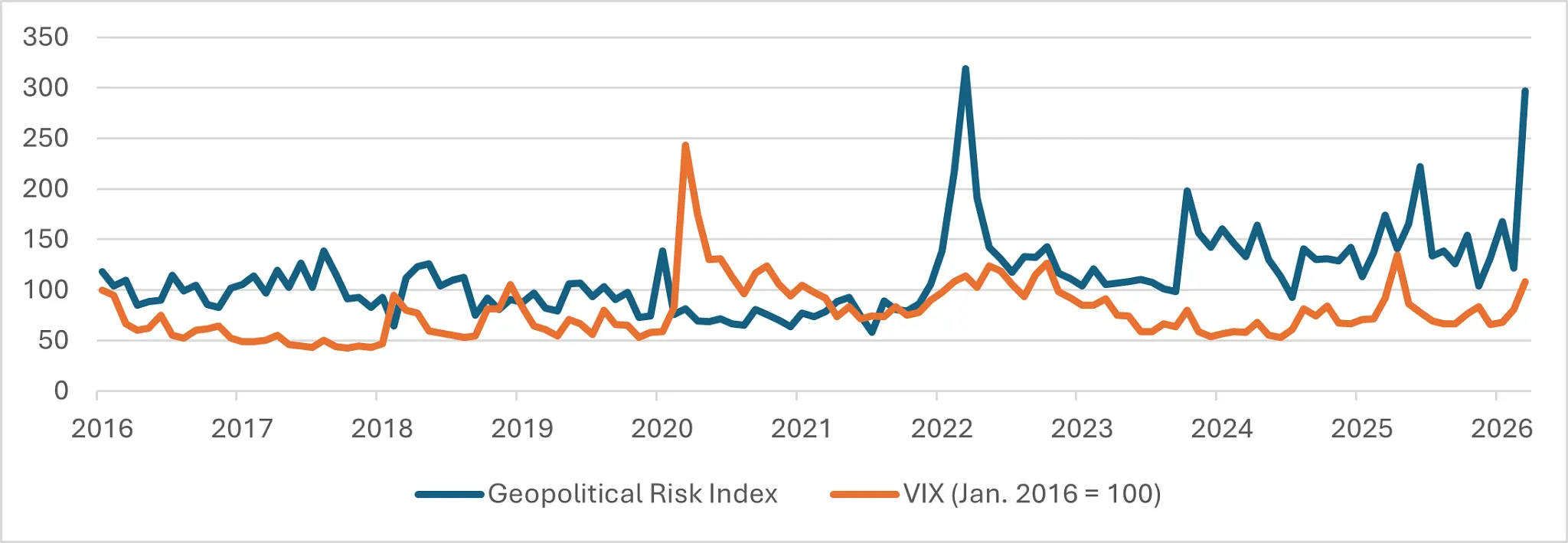

From an investment perspective, the evolving conflict has unsettled global markets and increased volatility as geopolitical risk has risen (Exhibit 1). Navigating periods where markets are reacting to tweets requires looking through the noise and staying focused on underlying medium- to long-term fundamentals. The conflict will have real implications for domestically focused UK companies. Yet, when you’re investing in UK equities, the UK economy is only one concern given the truly global nature of the market.

Exhibit 1: Market Volatility

Source: International Monetary Fund as at 30 April 2026. Chapter 1 Global Prospects and Policies. https://www.imf.org/-/media/files/publications/weo/2026/april/english/ch1.pdf

Domestic Challenges

Just as the UK had been set to recover from a second inflationary peak, it’s now approaching its third amid blockades to shipping through the Strait of Hormuz. In turn, as inflation picks up, so does the uncertainty around the path of interest rates. At the start of the year, markets had been pricing in further rate cuts, but expectations have swung sharply towards rate rises this year. We view this repricing as excessive. History suggests that oil price shocks alone do not typically trigger recessions; rather, economic downturns tend to occur when such shocks are compounded by aggressive monetary tightening. We think further rate cuts in the year ahead are now unlikely but remain cautious about the extent to which current rate-rise expectations will ultimately be realised.

As the UK faces down higher energy led inflation and an uncertain future path of interest rates, both the Organisation for Economic Co-operation and Development (OECD) and International Monetary Fund (IMF) have downgraded their UK growth forecasts. We would agree with a softer outlook for the UK, something that will weigh most heavily on domestically focused UK equities. However, we also recognise the UK is often viewed with excess pessimism and has the potential to surprise on the upside.

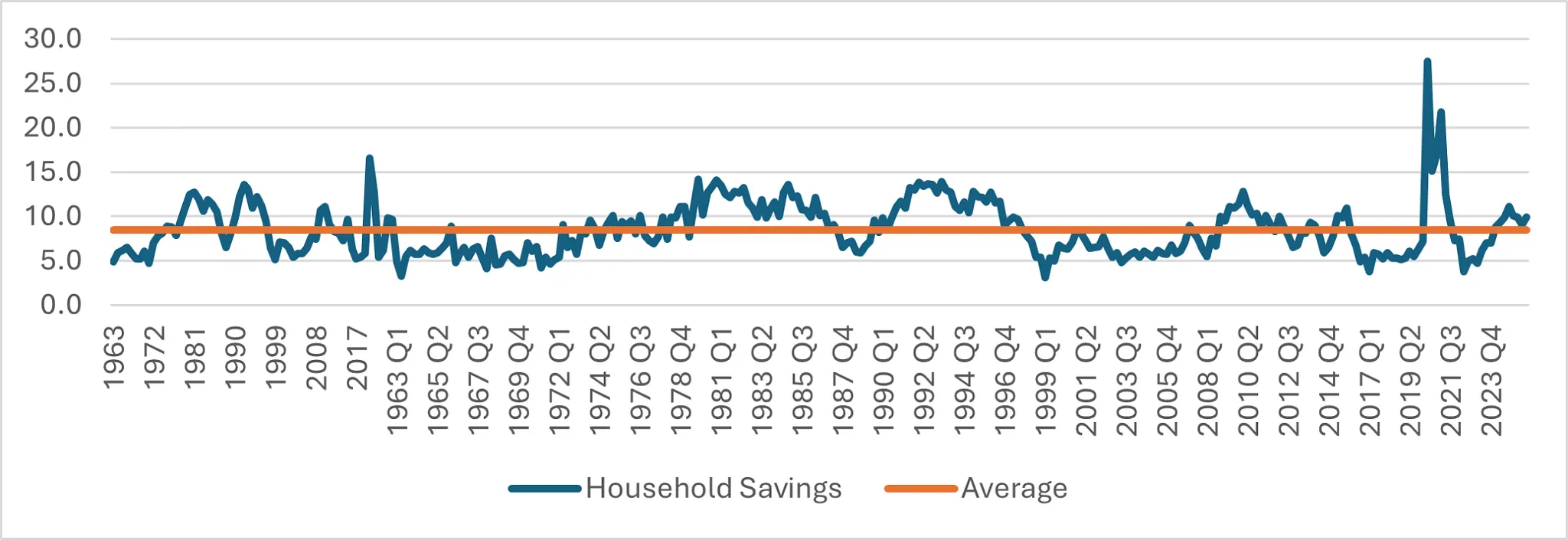

We would particularly point to the resilience of the UK consumer. Yes, high inflation will certainly put pressure on discretionary spending. However, on aggregate, household saving rates remain above long-term averages (Exhibit 2), which will act as a buffer, helping households remain resilient through the coming inflationary period.

Exhibit 2: Household Saving Rate2

Source: ONS as at 31 March 2026.

-

"Ultimately, the UK continues to be extremely well valued compared with global equities."

Investment Opportunities

As global conditions become more challenging, the UK market typically exhibits lower-beta characteristics and can provide more resilience during volatility. The market retains a relatively defensive profile through a large exposure to less-cyclical sectors such as utilities, health care and consumer staples. Moreover, UK equities are truly global with over 70% of the FTSE 100 Index revenues earned overseas1. Therefore, any domestic challenges should have a relatively low correlation with the operational performance of large cap UK listed companies.

The UK is also known for its attractive dividend yields. Given that income is a significant part of UK equity returns, this helps with downside protection in more volatile markets. Furthermore, in recent years dividend payouts have been complemented by an increasing use of share buybacks. Companies have been able to sustain both dividend payouts and share buybacks due to strong cash generation and healthy balance sheets. At the heart of our investment approach, we focus on profitable companies with strong balance sheets. Ultimately, well-capitalised companies with resilient business models are best placed to navigate the year ahead.

Of course, with investments, decision making always comes back to valuations. Ultimately, the UK continues to be extremely well valued compared with global equities. Especially when you consider that the UK market provides substantive global exposure. This valuation differential both offers significant potential upside but also offers an additional margin of downside protection when investing through uncertain times.

Fundamentals remain

In short, the Middle East conflict has injected renewed uncertainty into the outlook, but it has not changed the fundamental attractions of UK equities. The market combines substantial overseas earnings exposure with a defensive sector mix, attractive income and increasing buybacks—while valuations remain compelling versus global peers. In this environment, we believe a selective focus on profitable, well-capitalised companies with resilient business models offers the best way to navigate volatility and capture long-term opportunity.

Sources

1Source: Bank of England as at 18 December 2025.

2Source: ONS as at 31 March 2026.

3Source: Morningstar as at 31 January 2026.

Important Information

This information is issued and approved by ClearBridge Investment Management Limited (‘CIML’), authorised and regulated by the Financial Conduct Authority. It does not constitute investment advice. Market and currency movements may cause the capital value of shares, and the income from them, to fall as well as rise and you may get back less than you invested.

The information contained in this document has been compiled with considerable care to ensure its accuracy. However, no representation or warranty, express or implied, is made to its accuracy or completeness. ClearBridge Investments has procured any research or analysis contained in this document for its own use. It is provided to you only incidentally and any opinions expressed are subject to change without notice.

This document may not be distributed to third parties. It is confidential and intended only for the recipient. The recipient may not photocopy, transmit or otherwise share this document, or any part of it, with any other person without the express written permission of Martin Currie Investment Management Limited.

The document does not form the basis of, nor should it be relied upon in connection with, any subsequent contract or agreement. It does not constitute, and may not be used for the purpose of, an offer or invitation to subscribe for or otherwise acquire shares in any of the products mentioned.

Past performance is not a guide to future returns.

The distribution of specific products is restricted in certain jurisdictions, investors should be aware of these restrictions before requesting further specific information.

The views expressed are opinions of the portfolio managers as of the date of this document and are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. These opinions are not intended to be a forecast of future events, research, a guarantee of future results or investment advice.

Please note the information within this report has been produced internally using unaudited data and has not been independently verified. Whilst every effort has been made to ensure its accuracy, no guarantee can be given.

The information provided should not be considered a recommendation to purchase or sell any particular strategy / fund / security. It should not be assumed that any of the securities discussed here were or will prove to be profitable.

It is not known whether the stocks mentioned will feature in any future portfolios managed by ClearBridge Investments. Any stock examples will represent a small part of a portfolio and are used purely to demonstrate our investment style.

Risk warnings – Investors should also be aware of the following risk factors which may be applicable to the strategy shown in this document.

- Investing in foreign markets introduces a risk where adverse movements in currency exchange rates could result in a decrease in the value of your investment.

- This strategy may hold a limited number of investments. If one of these investments falls in value this can have a greater impact on the strategy’s value than if it held a larger number of investments.

- Smaller companies may be riskier and their shares may be less liquid than larger companies, meaning that their share price may be more volatile.