Content navigation

Key Takeaways

- Emerging market equities are thriving following more than a decade of underperformance.

- Valuations remain attractive, the macroeconomic backdrop is supportive and increased positive market sentiment should drive the asset class forward.

- Structural market drivers remain, with technology surging on strong earnings, China recovering and India offering long term opportunities.

2025 had been lining up to be a challenging year for emerging market (EM) equities. We witnessed growing global trade tensions following the U.S. Liberation Day tariff announcements, before the economic backdrop took a sharp turnaround for the better. A de-escalation of trade wars, a falling U.S. dollar and macroeconomic stabilization of China all marked positive news for EM equities, resulting in a strong year for the asset class as investors have been rewarded with impressive returns of over 30% through mid-November.

Following over a decade of underperformance, the tides have now turned, and we believe the EM market recovery is at an early stage. Valuations are appealing, global macroeconomic drivers are supportive and local structural and company-level opportunities all point toward significant upside potential for the asset class.

Macro Tailwinds Powering the EM Recovery

Emerging markets — a collection of individual countries, with differing economic, political and corporate backdrops — have one thing in common: their reliance on the U.S. economy. 2025 was yet another reminder of this as the U.S. demonstrated steady positive economic performance, combined with a weaker U.S. dollar and rate cuts in the second half, creating ideal conditions for EM equity performance.

EM equities typically benefit from a stable or depreciating U.S. dollar (Exhibit 1) because of lower U.S.-denominated debt servicing costs, commodity exporter tailwinds and increased monetary policy flexibility, which can facilitate lowering rates and supporting economic growth. All indications suggest this supportive dollar environment will remain in 2026. The Federal Reserve is forecast to continue cutting rates (Exhibit 2), suggesting the environment will become even more supportive of EM equities.

Exhibit 1: MSCI EM and U.S. Dollar Index Performance

As of Sept. 30, 2025. Source: FactSet.

Exhibit 2: U.S. Fed Funds Target Rate

As of Sept. 30, 2025. Source: FactSet.

International asset flows are also critical in driving prices for EM markets. The opportunity offered by lower valuations, combined with stronger economic growth and improving investor sentiment, creates a virtuous cycle attracting increased foreign capital flows. In turn, this further enhances potential investment performance. We’re still at an early stage in this process and anticipate increased foreign investments into EM equities over the coming years. In the meantime, we are bullish on three major themes in the year ahead: China, technology and India.

-

"While the U.S. is the first place many investors think of for tech investment, EM also offers the opportunity to invest in world-class companies with cutting-edge technological innovation. "

China: Quality and Growth at a Discount

The Chinese economy has begun to demonstrate increased stability, with trade tensions easing, exports remaining strong and a generally more optimistic outlook emerging. Our earlier belief that China wouldn’t separate much from the global economy has proven true, as relationships have improved and investors have regained confidence.

China’s policy pivot from a focus on deleveraging toward targeting growth has been gentler than anticipated, and the government has implemented mild stimulus measures focused on stabilizing the property sector to avoid overstimulating the broader economy. As a result, we are seeing a divergence in economic performance, with exporters and the industrial sectors booming and consumer demand and the property market subdued and drifting lower, respectively. While we don’t anticipate major economic stimulus, we do expect a continuation of targeted policy adjustments. The real opportunity lies in those pockets of the economy that are still thriving, particularly within technology, innovation and export-oriented businesses.

The recent strong performance of Chinese equities has not eliminated the significant valuation upside for high-quality, high-growth businesses. While the broader Chinese market has rebounded, many Chinese stocks remain near five-year valuation lows, suggesting substantial re-rating potential. We believe active equity managers are well-suited to thrive in this current market environment.

Technology: Undervalued EM Tech Poised for Catch-Up

While the U.S. is the first place many investors think of for tech investment, EM also offers the opportunity to invest in world-class companies with cutting-edge technological innovation. Many are benefiting from substantial investment in research and development and intellectual property creation. EM tech is best known for providing exposure to key global supply chain components for tech hardware. However, its growing reputation for world-leading innovation was further bolstered in 2025 with the launch of China’s DeepSeek chatbot, which sent shockwaves around the world as it shone a light on Chinese advancement in cutting-edge artificial intelligence (AI).

Technology investment in emerging markets can be found across industries; we see opportunities in areas such as industrial automation, e-commerce and fintech, as well as technological advancement driving increased global power demand amid the electrification of transport, heating and industry. This increased demand is further accelerating with the increasing energy demands from AI data centers. However, the old power networks are not ready or capable of meeting these increased electricity needs, meaning critical infrastructure investments are required.

As we look forward to 2026, the U.S. technology sector is currently trading at 31x forward P/E providing concerns to many market participants. This contrasts starkly with EM technology stocks, which trade at only 18x. These same EM tech stocks have forecast earnings that are expected to outpace their U.S. counterparts over the next three years.

India: Opportunity Despite Recent Underperformance

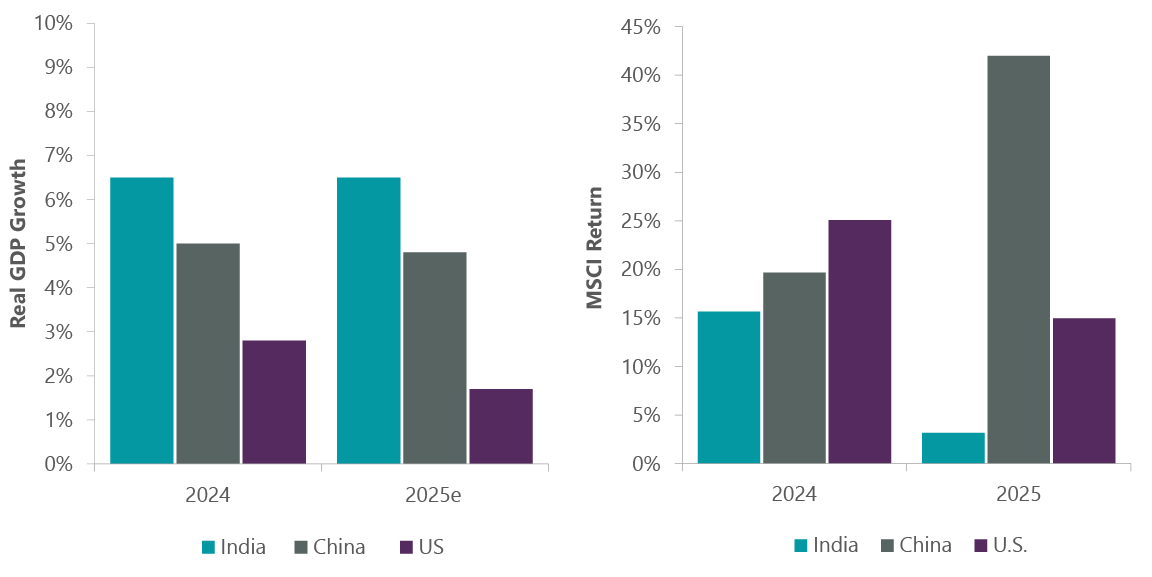

2025 has been a challenging year for Indian equities after a sharp valuation pullback following the 2024 election, negative economic growth revisions and consumer softness. However, the long-term investment case remains robust. India offers great upside potential as it benefits from a large and young population, and it remains the fastest-growing major global economy, with real GDP growth of 6.6% compared to 4.2% for EM overall (Exhibit 3). Indian valuations have seen a correction back to long-term levels (Exhibit 4), reinforcing the importance of active management to gain exposure to company-level opportunities. We see long-term opportunities in Indian banks, consumer discretionary stocks as well as the IT services industry, which is beginning to exhibit signs of stabilization from negative sentiment around AI risks.

Exhibit 3: Despite Equity Weakness, India Remains Fastest Growing Economy

Note: The indices used are as follows: India – MSCI India Index; China – MSCI China Index; U.S. – MSCI USA Index. Data as of Oct. 6, 2025. Source: FactSet.

Exhibit 4: India Valuations Back to Average

As of Oct. 22, 2025. Source: MSCI.

Conclusion

Investments in emerging markets equities aren’t simply a play on global macroeconomic factors and international asset flows. They also provide exposure to many countries offering economic growth rates faster than most developed nations and long-term structural trends such as an expanding middle class consumer and favorable demographics in select markets that can help drive company returns.

EM equities have turned a corner, showing strong performance after years of lagging returns. As the environment remains favorable, we believe the outlook for the asset class is positive, with further growth and re-rating potential on the horizon for investors willing to take a selective, stock-driven approach.

Important Information

This information is issued and approved by ClearBridge Investment Management Limited(‘CIML’), authorised and regulated by the Financial Conduct Authority. It does not constitute investment advice. Market and currency movements may cause the capital value of shares, and the income from them, to fall as well as rise and you may get back less than you invested.

The information contained in this document has been compiled with considerable care to ensure its accuracy. However, no representation or warranty, express or implied, is made to its accuracy or completeness. ClearBridge Investments has procured any research or analysis contained in this document for its own use. It is provided to you only incidentally and any opinions expressed are subject to change without notice.

This document may not be distributed to third parties. It is confidential and intended only for the recipient. The recipient may not photocopy, transmit or otherwise share this [document], or any part of it, with any other person without the express written permission of ClearBridge Investment Management Limited.

The document does not form the basis of, nor should it be relied upon in connection with, any subsequent contract or agreement. It does not constitute, and may not be used for the purpose of, an offer or invitation to subscribe for or otherwise acquire shares in any of the products mentioned.

Past performance is not a guide to future returns.

The distribution of specific products is restricted in certain jurisdictions, investors should be aware of these restrictions before requesting further specific information.

The views expressed are opinions of the portfolio managers as of the date of this document and are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. These opinions are not intended to be a forecast of future events, research, a guarantee of future results or investment advice.

Please note the information within this report has been produced internally using unaudited data and has not been independently verified. Whilst every effort has been made to ensure its accuracy, no guarantee can be given.

Risk warnings – Investors should also be aware of the following risk factors which may be applicable to the strategy shown in this document.

- Investing in foreign markets introduces a risk where adverse movements in currency exchange rates could result in a decrease in the value of your investment.

- This strategy may hold a limited number of investments. If one of these investments falls in value this can have a greater impact on the strategy’s value than if it held a larger number of investments.

- Smaller companies may be riskier and their shares may be less liquid than larger companies, meaning that their share price may be more volatile.

- Emerging markets or less developed countries may face more political, economic or structural challenges than developed countries. Accordingly, investment in emerging markets is generally characterised by higher levels of risk than investment in fully developed markets.

- Index futures and FX forwards